Obtaining a mortgage is an important stage in the home-buying process for the majority of prospective homebuyers.

Mortgages are often substantial loans with extended loan terms, so knowing how a mortgage works will help you better manage the borrowing process, whether you’re a first-time purchaser or a seasoned homeowner.

You want to make certain that you obtain the best home loan possible.

What Exactly Is a Mortgage?

A mortgage is a loan obtained from a lender to fund the purchase of a house. By signing a mortgage agreement, you pledge to pay back the borrowed funds at an agreed-upon interest rate.

It’s like the $10,000 credit card limit only in this case you’ve already spent that notional amount to buy a house and now you have to pay back the borrowed money.

The house serves as collateral. That is, if you fail to repay your mortgage, the bank has the authority to foreclose on your home.

Your loan does not become a mortgage until it is attached as a lien to your property, which means that your ownership of the home is conditional on you repaying your new loan on time and according to the conditions you agreed to.

You repay part of what you borrowed, plus interest, each month. Failure to repay the mortgage might result in foreclosure.

Mortgages are also significantly more durable than other forms of borrowing, with 30-year mortgages being the most frequent.

Mortgages normally ask you to make an initial payment — known as the down payment — and then repay the remainder over time.

How Does It Work?

The principle is the amount borrowed from your mortgage. A portion of your monthly payment will be used to pay down the main, or mortgage debt, and part will be used to pay interest on the loan.

The lender charges you interest for lending you money. Until the mortgage is paid in full, the lender maintains legal title to the property.

A mortgage differs from other types of loans in that if you fail to repay the loan, your lender may sell your property to collect its losses.

Compare that to what happens if you don’t make your credit card payments: You are not required to return the items purchased with the credit card, but you may be required to pay late penalties to keep your account current, in addition to dealing with bad effects on your credit score.

Many programs help people pay off their mortgage or take it at a lower interest rate or not make a down payment but a particular program may be limited by the state you live in and certain conditions you must meet.

Important Mortgage Terminology to Understand

Prospective homeowners may encounter some unfamiliar words. Here is a list of some of the most prevalent terms and their definitions.

APR

The term “annual percentage rate” is often shortened to “APR.” Because it combines your interest rate with fees, points, and other lender charges, this figure indicates the overall cost of borrowing money to purchase a property.

Examining the APRs that various lenders provide is another approach to evaluating expenses.

Debt-to-income ratio (DTI)

A crucial consideration for mortgage lenders while reviewing your loan application. It is the proportion of your total monthly revenue that is allocated to debt payments.

Lenders normally want a DTI of less than 43%, however certain lending programs allow up to 50%.

Loan Amount

The amount borrowed to meet the remaining purchase price. Your loan amount will be the selling price of the house less your down payment.

Mortgage Protection Insurance

Mortgage insurance protects a lender from damages incurred if they have to foreclose on your house due to nonpayment. Mortgage insurance is required on certain government-backed loans regardless of down payment, but it is not required on conventional loans with a 20% or higher down payment.

Down payment

The monetary contribution you make to the purchase. Lenders often demand a down payment of 3% to 5% of the purchase price, but many buyers strive for a 20% down payment to avoid paying mortgage insurance.

Closing

When it comes to purchasing a property, the term “closing” has two distinct but connected connotations.

It may refer to the period between applying for a mortgage and signing the papers and getting the keys, or it can refer to the day the loan “closes.”. In recent times, electronic closing is introduced by various states like Colorado, Connecticut, Delaware, Hawaii, etc.

How to Get Approved For a Mortgage

A lender will use your job history and credit history to determine how likely you are to repay your loan. The past two years of your credit history should be free of late payments since lenders want to see steadiness.

The better your credit, the cheaper your interest rate and mortgage payment. Mortgage lenders provide the greatest interest rates to consumers with good credit and large down payments.

Lenders seek two years of consistent work with a single job (or at least employment in the same field).

Other income is admissible if it has a two-year history, such as earnings from part-time or freelance work, overtime, bonuses, or self-employment.

Your DTI helps lenders assess your ability to make loan repayments and manage the monthly mortgage payment.

As a general rule, a lower DTI is always preferable. The Consumer Financial Protection Bureau, on the other hand, advises a DTI of 43% or below.

You may start working with a bank, credit union, online lender, or mortgage broker as soon as you’re prepared to apply.

A lender determines a mortgage preapproval to show the amount you may borrow, the kind of loan, and the interest rate you are likely to qualify for.

If you are confident in the previous stages, then all you have to do is compare offers, choose the most profitable for you, and start and finish paying off your mortgage.

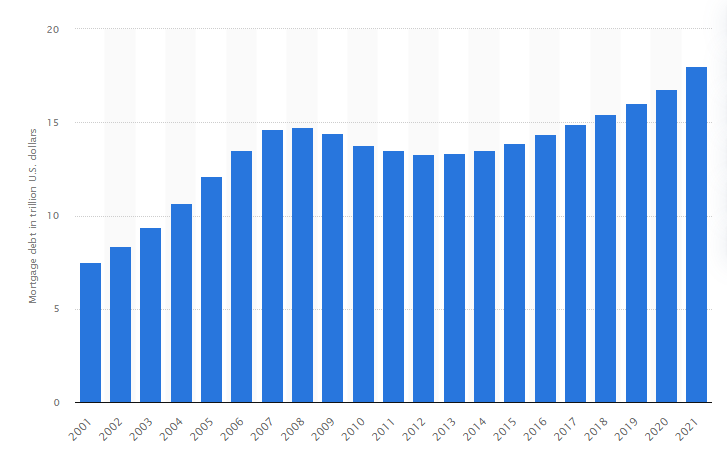

In recent years, the overall amount of mortgage debt in the United States has risen. Mortgage debt reached 18 trillion US dollars in 2021, up from 16.8 trillion US dollars in 2020, because prices are rising and demand is not falling.

Value of mortgage debt outstanding in the United States from 2001 to 2021

Despite the constant crises at present, people take mortgage loans and actively pay them off. If you are confident that you can pay off the mortgage and own the house, then don’t waste your time.

Conclusion

It’s not simple or inexpensive to become a homeowner, but it’s well worth the effort. Before you enter the mortgage market, you must educate yourself on what a mortgage is.

You must be well prepared for a mortgage and choose the finest deal.